Prefer to listen instead? Check out the audio version of this article

Most CPG brands ask their TPM vendor two questions about compliance: "Do you have SOC 2?" and "Can you fill out our security questionnaire?"

Those questions aren't wrong. But they're incomplete, and the gap between what you ask and what you should ask is where financial reporting risk lives.

This is a practical guide for CPG finance, audit, and procurement teams who are actively evaluating a trade promotion management platform or want to pressure-test the one they already use. It covers the specific questions to ask, what the answers should look like, and how to interpret what vendors tell you.

When procurement teams evaluate SaaS vendors, they typically run one of two processes: a vendor security questionnaire (VSQ) or a review of the vendor's SOC 2 report. Both are useful, but neither is sufficient for a TPM platform.

Here's why: VSQs are self-reported. SOC 2 covers security and operational controls. But trade promotion software doesn't just store your data, it processes data that flows directly to your income statement. Accruals, deductions, revenue recognition, off-invoice allowances. These aren't operational records. They're financial records.

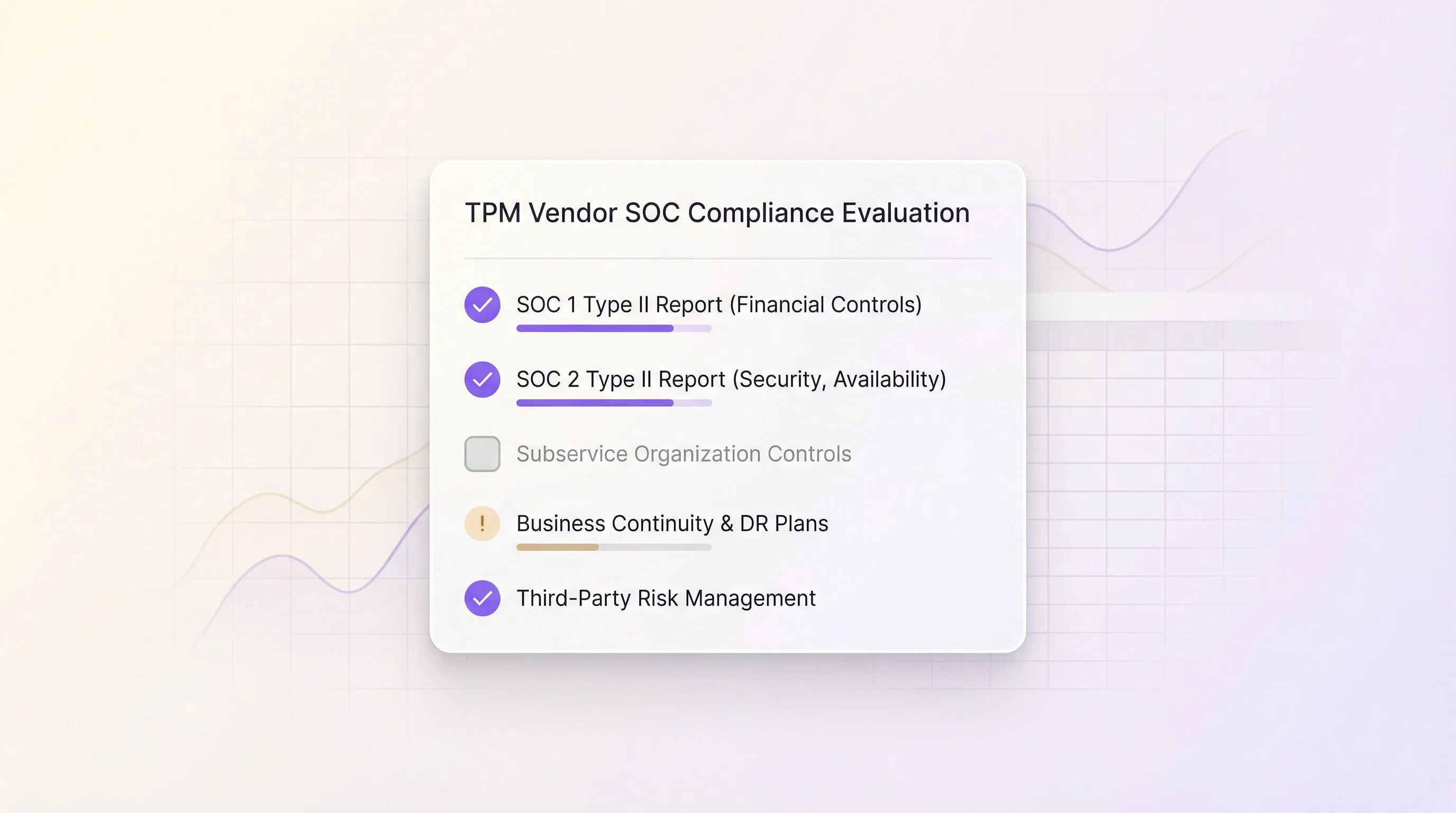

The compliance standard designed for this category of risk is SOC 1 — specifically, SOC 1 Type 2. And the majority of TPM vendors either don't have it, or don't understand why it matters.

This is the question most brands don't think to ask. SOC 1 audits the financial controls inside a platform, i.e. the controls governing how accruals are processed, how adjustments are logged, how approvals are documented, and how audit trails are maintained.

Type 2 specifically means the auditor assessed those controls over a 6–12 month period, not just at a single point in time. A vendor with only SOC 1 Type 1 can tell you their controls were designed correctly on a given day. They can't tell you those controls worked reliably over time.

What a good answer looks like: "Yes, we have SOC 1 Type 2. Here's our most recent report. Our audit period covers [X months] and was conducted by [named CPA firm]."

Red flag: "We're working toward SOC 1." "We have SOC 1 Type 1." "We haven't needed it, our customers haven't asked." This tells you the platform wasn't built with financial system rigor in mind.

Not all SOC 1 reports are scoped the same way. A vendor can technically hold a SOC 1 certification while scoping it so narrowly that it doesn't cover the financial processes most relevant to you.

For a TPM platform, the SOC 1 scope should cover:

What a good answer looks like: A vendor who can walk you through their control objectives and explain which financial processes are in scope without hesitation.

Red flag: Vague answers ("it covers our financial systems"), inability to share the scope, or a report that predates significant product changes.

SOC reports must be issued by a licensed CPA firm following AICPA standards. Audit quality varies by firm. More importantly, audit currency matters - a SOC report from 18 months ago tells you about controls that may have changed significantly since.

What a good answer looks like: A named, reputable CPA firm. An annual audit cycle. A current report (issued within the last 12 months).

Red flag: An audit firm you can't verify. A report older than 12 months. A vendor who says their last report "is being updated."

SOC 2 Type 2 is the baseline security standard for enterprise SaaS. For a TPM platform storing retailer contracts, promotional data, and consumer information, it's non-negotiable.

The five Trust Services Criteria are: Security, Availability, Processing Integrity, Confidentiality, and Privacy. Most vendors cover Security at minimum. The others vary.

What a good answer looks like: SOC 2 Type 2 with at minimum Security, Confidentiality, and Availability, which are the criteria most directly relevant to a trade promotion platform.

Red flag: SOC 2 Type 1 only. No SOC 2 at all. A vendor who can only produce penetration test results or a self-completed CAIQ questionnaire as a substitute.

This is a behavioral question, not a documentation question. It reveals whether a vendor actually understands their own control environment, or just passed an audit.

A well-designed TPM platform should be able to explain: what triggers an alert when an accrual is changed outside a threshold, how approval workflows prevent unauthorized financial adjustments, how audit trails are stored and protected, and what recovery looks like if something goes wrong.

What a good answer looks like: A specific, confident explanation from someone who has direct knowledge of the platform's control design, not a generic answer about "enterprise-grade security."

Red flag: The sales team isn't sure who to loop in. The answer defaults to "our SOC report covers that." No one can describe the control workflow in plain terms.

If your existing TPM vendor can't produce a SOC 1 Type 2 report, that doesn't automatically mean you need to switch. But it does mean you have unmitigated financial controls risk and your finance and audit teams should understand that explicitly.

In the near term: ask your vendor directly whether they're pursuing SOC 1 and what their timeline looks like. Request any available documentation on their financial control environment. Flag the gap in your internal risk register.

Longer term: when SOC 1 Type 2 is unavailable, your own team carries the burden of validating that the platform's financial outputs are reliable. That's expensive, time-consuming, and may not be sufficient.

Vividly holds both SOC 1 Type 2 and SOC 2 Type 2 certifications.

In practice, that means:

When your audit team asks "how do we know this number is right?" — Vividly's answer is an independently verified one.

Ready to review our SOC reports or discuss how our compliance posture supports your audit readiness?

Discover a new vision for trade

.webp)

.webp)

.webp)

.webp)

.webp)